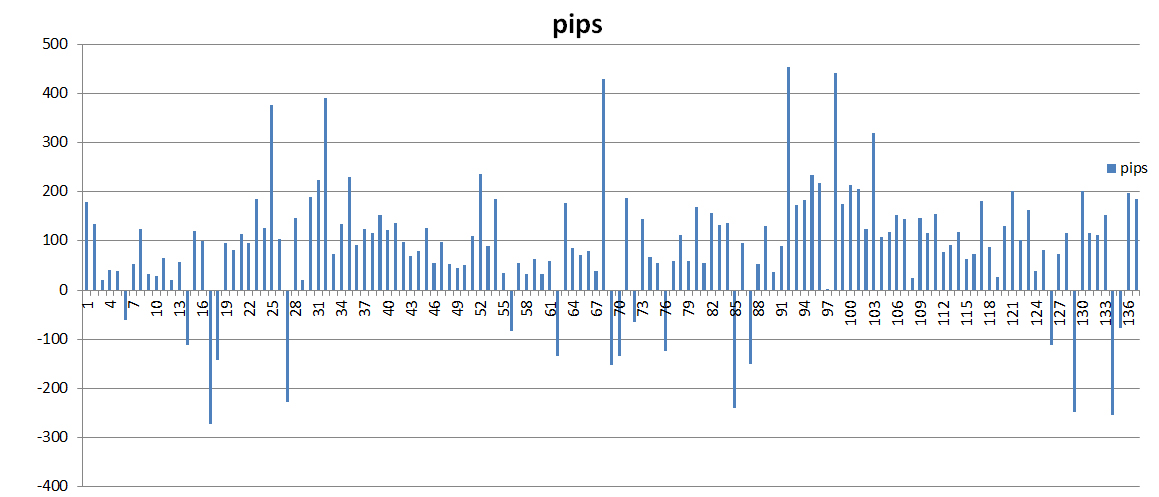

Trading system back testing

We have performed 10 years back testing for our mechanical trading system on the historical data

of EUR/USD pair, on daily chart, from 2001 till 2011.

The back testing has generated 137 trades with a compounded return +192.8%.

Profitability %: 89.5%

Maximum Peak to Trough DrawDown: -2%

Average Stop loss: 180 pips

Average Monthly return: +1.25%

Standard Deviation: 1.23%

Sharp Ratio: 3.30

Monthly VaR at 95% confidence level: -1%

Average Trade Life Span: 4 days